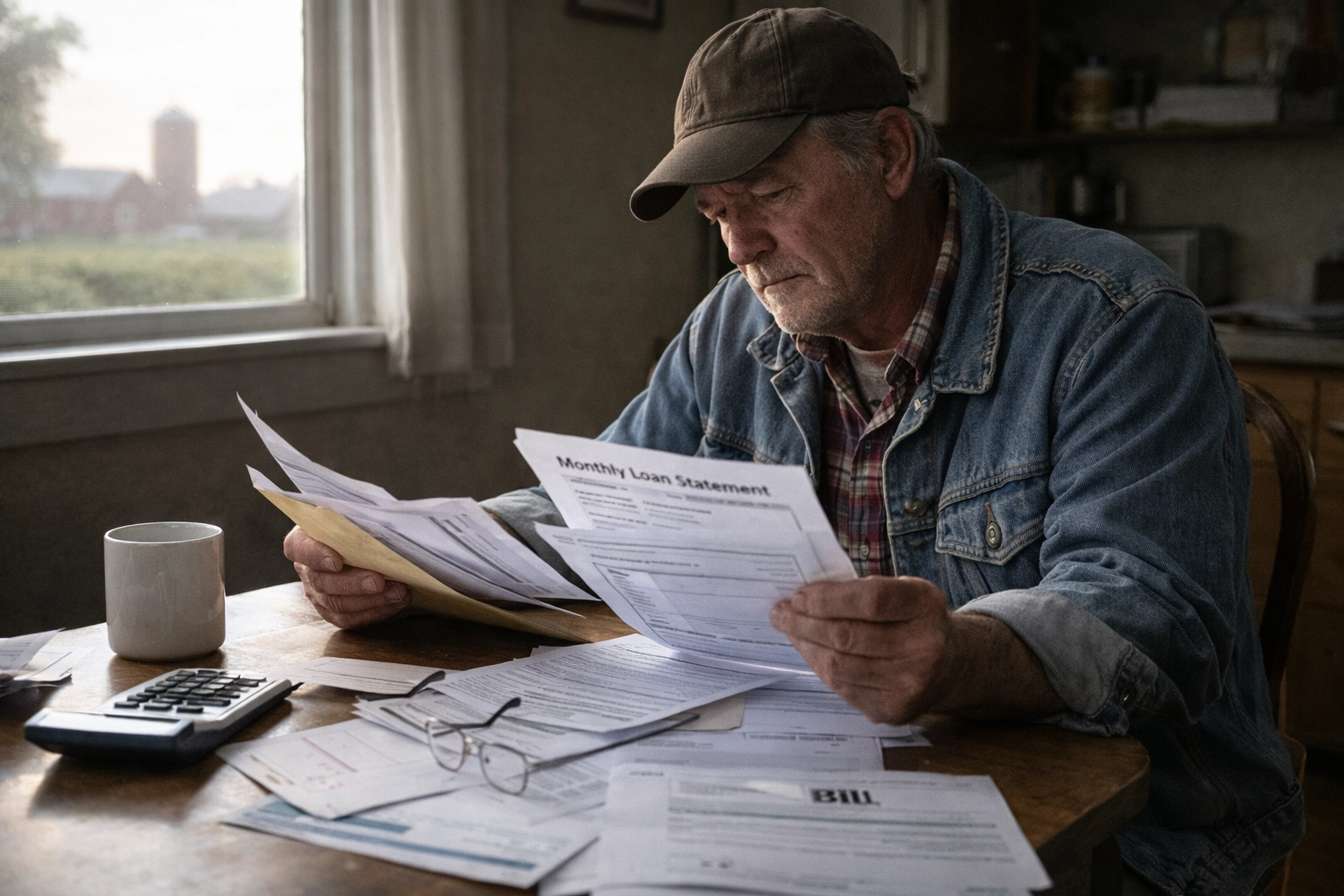

Pickup trucks idled along the edge of a frozen cornfield in central Iowa as farmers compared notes. The conversation had little to do with yields or weather outlooks. It centered on invoices. Fertilizer quotes that no longer seemed to move lower. Equipment payments recalculated after another interest-rate reset. A machinery upgrade delayed not for lack of confidence, but for lack of margin certainty.

This scene has become increasingly common across U.S. agriculture in 2026. The tension is subtle. Commodity prices remain workable by historical standards. Demand has not collapsed. Balance sheets, in aggregate, still look healthier than during previous downturns. Yet decision-making has grown more cautious. Planning horizons are shorter. Capital is rationed more carefully.

The pressure reshaping U.S. farm economics is not dramatic or headline-driven. It is cumulative. Costs that once rose and fell cyclically have reset structurally higher, and that shift is quietly altering how farms invest, expand, and manage risk.

A higher-cost baseline replaces mean reversion

For much of the past decade, producers could assume that spikes in input costs would eventually ease. That assumption has weakened. The inflation surge of the early 2020s left behind a new baseline for fertilizer, labor, machinery, and credit—one that shows little sign of reverting.

The U.S. Department of Agriculture projects that total farm production expenses will remain elevated through 2026, even as net farm income stabilizes after retreating from its 2022 peak.

This divergence matters. Net farm income is a snapshot. Costs define trajectory. Higher replacement expenses, rising depreciation, and more expensive capital mean that farms must generate more revenue simply to stand still. For many operations, the economic question is no longer whether they can operate profitably this season, but whether today’s cost structure supports reinvestment over the next decade.

What is emerging is not a sudden crisis, but a slow exposure of risk. In that context, “farm aid missing” has become less a slogan and more a description of the moment confronting US agriculture in 2026.

Fertilizer costs: relief without reset

Fertilizer markets illustrate the new reality. Prices for nitrogen, phosphate, and potash have fallen significantly from their crisis-era highs. They have not returned to pre-pandemic norms.

According to the Economic Research Service, fertilizer now accounts for a larger share of operating expenses for corn and wheat producers than at any point during the 2010s.

The reasons are structural. Energy markets remain volatile. Global fertilizer production is geographically concentrated and politically sensitive. Environmental compliance costs have increased. Even with softer demand, these factors anchor prices at a higher floor.

Producers have adjusted, but not without consequence. Variable-rate application, tighter nutrient management, and split nitrogen timing are now standard practice. Crop rotations increasingly factor input intensity alongside agronomics. These strategies improve efficiency, but they require capital, data, and management capacity—inputs that carry costs of their own.

Machinery prices extend depreciation cycles

Machinery markets have followed a similar arc. New equipment prices surged during supply chain disruptions and stabilized at higher levels. Used equipment prices adjusted upward. Repair costs climbed further as parts inflation and dealership labor rates increased.

The result is not a collapse in investment, but a stretching of depreciation cycles. Producers are running equipment longer, prioritizing maintenance over upgrades. For large operations, scale helps absorb these costs. For mid-sized farms, tradeoffs are sharper.

Financing new equipment at today’s interest rates raises fixed costs. Delaying replacement raises operational risk during narrow planting and harvest windows. Many producers are choosing the least disruptive option rather than the most productive one—a decision that quietly restrains productivity growth over time.

This is not the first time US agriculture has turned to federal support during a downturn. But the current moment feels different. The post-pandemic surge in farm income has faded.

Labor costs harden into constraint

Labor is no longer just an expense line. It has become a binding constraint. Rural wages have risen steadily as agriculture competes with construction, logistics, energy, and manufacturing. In specialty crops, availability matters as much as price.

H-2A wage rates continue to climb, and compliance costs compound the pressure. For fruit, vegetable, and dairy producers, labor availability increasingly determines acreage, crop choice, and harvest timing.

Credit programs administered through the Farm Service Agency can help manage operating cash flow,

but financing does not create workers. Automation offers partial relief, yet adoption remains uneven and capital-intensive.

The economic effect is gradual reallocation. Some labor-intensive production is pressured in high-cost regions. Other crops migrate toward areas with more stable labor pools or infrastructure better suited to mechanization. These shifts rarely register nationally, but they accumulate locally.

Interest rates amplify every other cost

Higher interest rates magnify all cost pressures. Borrowing no longer smooths volatility. Variable-rate debt resets faster than revenues adjust. New land purchases carry greater downside risk.

Many farms entered the mid-2020s with strong balance sheets, supported by asset appreciation and strong income years earlier in the decade. That cushion has delayed widespread distress. But sensitivity to rate movements has increased, particularly for younger producers and recent entrants.

Congressional hearings increasingly frame farm credit as a long-term competitiveness issue rather than a short-term emergency.

The emphasis is on access and stability, not broad relief.

Regional divergence sharpens beneath national averages

National income averages obscure widening regional divergence. Grain-dominant regions benefit from scale efficiencies and established logistics, even as input costs rise. Specialty crop regions face sharper labor and water cost exposure. Livestock producers absorb higher feed, veterinary, and environmental compliance expenses.

These pressures shape land values, rental rates, and consolidation trends. In some regions, higher costs accelerate consolidation as larger operators spread fixed expenses across more acres. In others, they encourage diversification into processing, direct marketing, or value-added channels.

The adjustment is uneven. There is no single response, only localized recalibration.

The latest federal funding package marks a clear departure. Farm aid—anticipated by many producers and closely watched by lenders—was excluded.

Technology shifts from promise to discipline

Technology adoption continues, but the narrative has changed. Precision tools are no longer sold primarily as yield enhancers. They are cost-containment instruments.

Variable-rate inputs, remote sensing, and predictive maintenance help reduce waste and stabilize margins. Yet technology carries its own costs—subscriptions, data integration, training. Returns vary widely by operation size and management capacity.

For many farms, the challenge is selectivity. Tools must simplify decisions, not complicate them. In 2026, technology must earn its place on the balance sheet.

Policy cushions volatility, not structure

Federal policy remains a stabilizing force, but fiscal constraints limit its reach. Rather than sweeping cost relief, policymakers emphasize risk management, conservation incentives, and credit access.

USDA analysis shows that while aggregate farm income remains above long-term averages, gains are unevenly distributed across commodities and regions. Policy reduces volatility. It does not reverse structural cost pressure.

Strategy under a higher-cost equilibrium

The cumulative effect of rising costs is strategic restraint. Expansion decisions slow. Lease terms tighten. Input purchases are timed with greater precision.

More subtly, the conversation on many farms has shifted from growth to durability. Can the operation withstand prolonged periods of higher costs without sacrificing soil health, labor stability, or succession plans? Can it invest selectively without overextending?

These are not defensive questions. They reflect adaptation to a new economic baseline.

The expanding role of the Department of Homeland Security in disaster response, infrastructure protection, and emergency funding has begun to overlap with traditional congressional authority over agricultural spending.

Looking ahead

Few signals suggest a return to the low-cost environment that defined much of the previous decade. Energy markets remain uncertain. Labor demographics are tightening. Capital costs are unlikely to retreat quickly.

The reshaping of U.S. farm economics in 2026 is therefore quiet but consequential. Its impact will be measured less by annual income figures than by which operations retain the flexibility to invest, innovate, and transition across generations under a permanently higher cost curve.

Written by Janardan Tharkar – an agriculture content researcher and blogging professional with practical experience in farming education, digital publishing, and SEO content optimization. Janardan focuses on modern U.S. agriculture trends, smart farming technologies, irrigation systems, crop development, organic farming practices, and farmer-support programs to create helpful, practical, and trustworthy content for American readers.