In 2026, fertilizer prices are not just rising — they are reshaping farm economics.

For many farmers, fertilizer is no longer just an input cost.

It is the difference between profit and loss.

So the real question is:

How are rising fertilizer prices changing the economics of farming?

Why Fertilizer Matters in Farm Economics

Fertilizer is one of the largest costs in modern farming.

In many cases, it accounts for 20–30% of total production expenses.

This means even small price increases can significantly impact profitability.

When fertilizer prices rise, farmers are forced to either:

- Increase investment

- Reduce usage

- Or accept lower margins

This makes fertilizer a key driver of farm economics.

How Fertilizer Prices Affect Profit

Farm profit depends on a simple equation:

Profit = Crop Price – Total Cost

In 2026:

- Crop prices are stable or slightly higher

- But fertilizer costs have increased sharply

This reduces the profit margin.

In some cases:

- Higher yield does not mean higher profit

- Because input costs are too high

This is why many farmers are focusing on return per dollar — not yield alone.

When input costs stop being “inputs” and start becoming constraints

Fertilizer has always been central to modern agriculture, but in 2026 it has become the dominant marginal cost driver—especially for nitrogen-intensive crops like corn.

Recent data illustrates the magnitude of this shift:

- Urea prices surged to around $600 per ton in early 2026, with double-digit monthly increases

- U.S. corn fertilizer costs are projected at ~$166 per acre, rising year-over-year

- Global fertilizer prices rose ~20% in 2025 and remain structurally elevated

At the same time, crop prices are not rising proportionally. According to World Bank commodity outlooks, agricultural prices are expected to remain broadly stable into 2026

That mismatch—rising input costs against flat output prices—is the core economic tension reshaping farm economics.

Historically, fertilizer was a “scalable input”—farmers could increase or decrease usage based on expected returns. In 2026, it is becoming a binding constraint. Farmers are not just optimizing yields; they are optimizing survival margins.

The energy–fertilizer–agriculture chain tightening

To understand why fertilizer prices have become so structurally disruptive, you have to move upstream—to energy.

Nitrogen fertilizers are essentially “natural gas in solid form.” Their production depends heavily on natural gas as both feedstock and energy source. This creates a tight linkage:

Energy shock → Fertilizer cost spike → Farm input inflation → Food price pressure

In 2026, this linkage has intensified due to geopolitical disruptions. Energy market volatility and supply risks are well documented in global coverage (for example: https://www.reuters.com/business/energy/iran-wars-energy-impact-forces-world-pay-up-cut-consumption-2026-03-21/).

This is structurally important for two reasons:

- Dual exposure risk

Farmers are exposed not only to fertilizer price volatility but also to fuel and logistics costs—both tied to energy markets. - Cost synchronization

Unlike past cycles where different input costs moved independently, 2026 is characterized by synchronized cost inflation—fertilizer, fuel, and transport rising together.

The result is a compression of farm margins that is far more severe than isolated input shocks.

As input costs continue to rise, decisions around nitrogen application are becoming less about maximizing yield and more about managing financial risk. This shift reflects a broader pressure across U.S. corn farming, where weather uncertainty and cost volatility are forcing farmers to rethink traditional strategies. A deeper look at this challenge can be found in

corn farmers under pressure in 2026: costs, weather, and planting strategy, where these economic and environmental factors come together to shape on-field decisions.

Corn vs soybeans: the microeconomic pivot point

Nowhere is this more visible than in crop choice decisions.

Corn is highly nitrogen-intensive. Soybeans, by contrast, fix nitrogen biologically and require significantly less fertilizer. When fertilizer prices rise sharply, the relative economics shift.

This is already happening in 2026:

- Farmers are reducing nitrogen application rates

- Some are switching acreage from corn to soybeans

- Others are accepting lower yield potential to control costs

On-the-ground reporting confirms that farmers are actively adjusting planting strategies due to fertilizer costs.

From a microeconomic perspective, the decision framework has changed:

Before (Yield Maximization Model):

Maximize output per acre using optimal fertilizer rates

Now (Cost-Constrained Optimization):

Maximize profit under input cost uncertainty

This distinction is critical. Yield is no longer the primary objective—input efficiency and risk management are taking center stage.

How Fertilizer Prices Affect Profit

Farm profit depends on a simple equation:

Profit = Crop Price – Total Cost

In 2026:

- Crop prices are stable or slightly higher

- But fertilizer costs have increased sharply

This reduces the profit margin.

In some cases:

- Higher yield does not mean higher profit

- Because input costs are too high

This is why many farmers are focusing on return per dollar — not yield alone.

The yield paradox: cutting costs, reducing output

Reducing fertilizer use is not a neutral decision—it directly affects yields.

This creates a structural paradox:

- High fertilizer prices → lower application rates

- Lower application rates → reduced yields

- Reduced yields → tighter supply

- Tighter supply → upward pressure on prices

But demand is not infinitely elastic.

If global demand is stable—as current projections suggest—price increases may not fully compensate for yield losses. This creates a scenario where:

Farmers earn less even when prices rise

The Food and Agriculture Organization tracks this dynamic through its Food Price Index , which shows only moderate food price increases relative to input cost pressures.

In other words, the system is absorbing cost shocks through margin compression, not full price transmission.

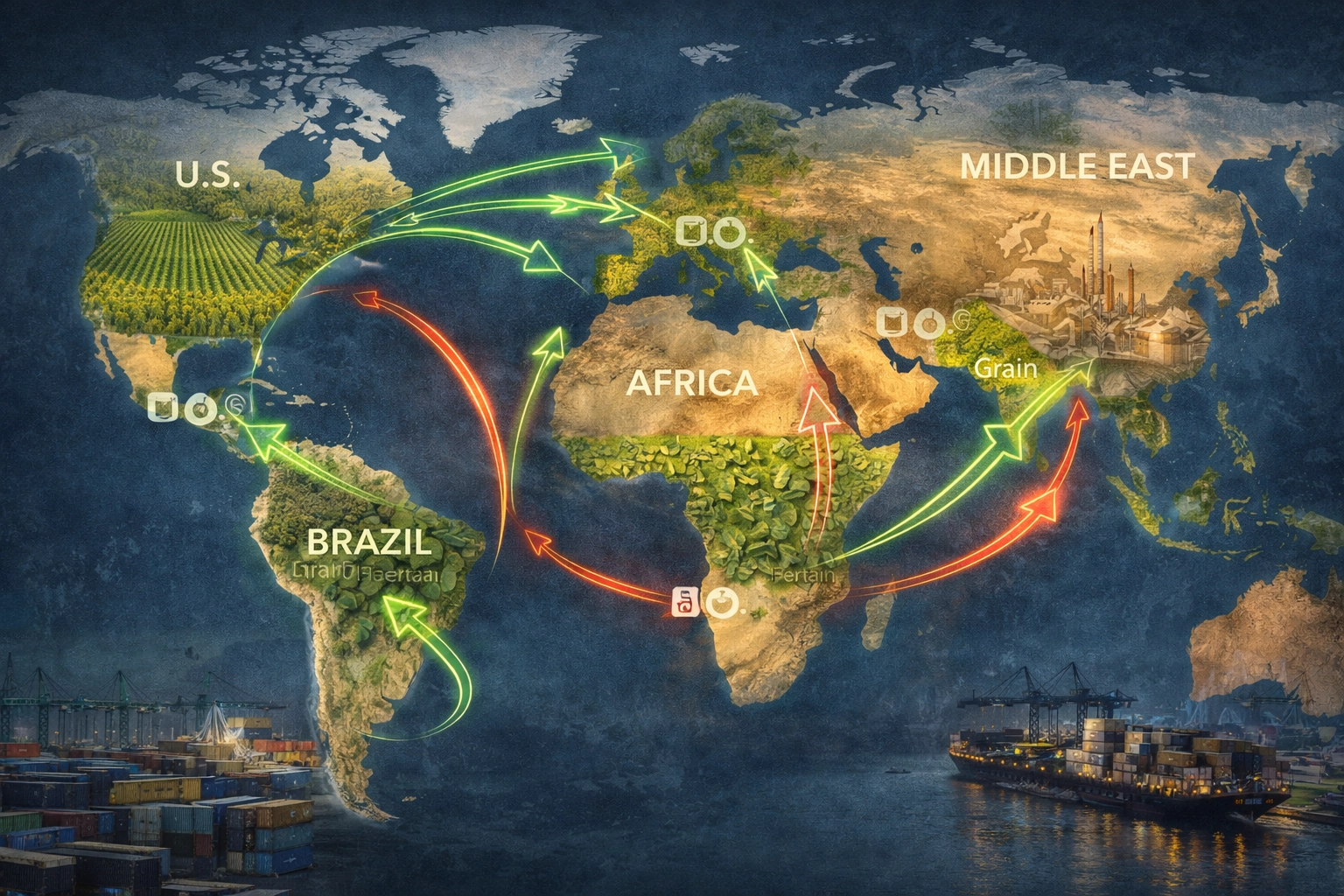

Global ripple effects: from Midwest fields to world markets

The structural impact extends far beyond the U.S.

Fertilizer is one of the most globally traded agricultural inputs, with supply concentrated in a few regions. Disruptions—whether geopolitical, logistical, or energy-related—quickly propagate worldwide.

Recent developments show:

- Significant portions of global fertilizer trade affected by geopolitical tensions

- Countries like Brazil exploring alternative fertilizers and cost adjustments

- Developing nations facing increased food security risks

Coverage of these global disruptions highlights the scale of the issue (example: https://www.reuters.com/world/middle-east/war-iran-threatens-fresh-food-price-shock-across-developing-world-2026-03-20/).

This creates a layered global effect:

- Advanced economies (U.S., EU)

Absorb costs through reduced margins and efficiency gains - Emerging exporters (Brazil, Argentina)

Adjust input mix and cropping strategies - Import-dependent countries

Face direct threats to food security

The fertilizer market has effectively become a transmission mechanism for global inequality in agriculture.

While global supply estimates and market projections provide a broader outlook, the real impact of these shifts is felt at the field level. In regions like the U.S. Midwest, farmers are already facing difficult planting decisions due to excess soil moisture and narrow timing windows. This real-world challenge is explored in detail in

too wet to plant, too late to wait: the real decisions behind Midwest corn planting in 2026, where macro trends translate into high-stakes on-farm choices.

Trade competitiveness: the quiet erosion of U.S. advantage

The U.S. has historically enjoyed a cost advantage in agricultural production, supported by efficiency and scale. Research from USDA Economic Research Service highlights comparative cost structures in major crops

But that advantage is narrowing.

When fertilizer prices rise globally, the impact is not uniform:

- Regions closer to fertilizer production may have lower transport costs

- Countries with domestic production gain strategic advantage

- Export competitiveness becomes sensitive to input cost structures

If U.S. production costs rise faster than competitors, export margins shrink—even if global prices increase.

This is particularly important for corn, wheat, and feed grain markets, where small cost differences can shift global trade flows.

Inflation dynamics: why food prices don’t fully reflect input costs

One of the most counterintuitive aspects of 2026 is the disconnect between input inflation and food price inflation.

Despite rising fertilizer and energy costs, global agricultural prices are expected to remain relatively stable. The World Bank Commodity Markets Outlook explains this dynamic in detail .

This happens because:

- Demand constraints

Consumers cannot absorb unlimited price increases - Global supply buffers

Stock levels and diversified production moderate spikes - Policy interventions

Governments act to stabilize domestic food markets

The result is a partial transmission mechanism:

- Input costs rise sharply

- Output prices rise moderately

- Margins absorb the difference

This is fundamentally different from classical inflation cycles and has long-term implications for farm viability.

Short-term adjustment vs long-term structural change

In the short term, farmers respond tactically:

- Reduce fertilizer rates

- Delay purchases

- Lock in prices when possible

- Shift crop mix

These are adaptive responses.

But the long-term effects are structural:

- Precision agriculture adoption increases

- Biofertilizer and regenerative practices gain traction

- Countries invest in domestic fertilizer production

- Farm consolidation accelerates

- Input efficiency becomes the primary competitive advantage

Even if fertilizer prices soften slightly, long-term projections from institutions like the World Bank suggest they will remain above historical norms

A new economic equilibrium: agriculture under constraint

The old model of U.S. agriculture was built on:

- Abundant inputs

- Predictable cost structures

- Yield-driven profitability

The emerging model is defined by:

- Constrained inputs

- Volatile cost structures

- Efficiency-driven profitability

This transition is not temporary—it reflects a deeper restructuring of how agriculture functions under global economic pressure.

Across the U.S. Corn Belt, planting decisions are increasingly tied to market signals and policy expectations. As explored in our in-depth Corn Belt field analysis, these choices reflect a complex mix of agronomy, economics, and timing.

The deeper implication: fertilizer as a strategic variable

Fertilizer is no longer just an input—it is a strategic variable in global agriculture.

It influences:

- Crop choices

- Yield potential

- Trade competitiveness

- Food security

- Inflation dynamics

And perhaps most importantly, it determines who can produce—and who cannot.

How Farmers Can Manage Fertilizer Costs in 2026

Farmers must adapt to rising input costs with smarter strategies.

Key approaches:

- Optimize fertilizer application based on soil data

- Avoid overuse — focus on efficiency

- Consider crop rotation to reduce fertilizer demand

- Track fertilizer prices and buy at the right time

The goal is not to use less fertilizer blindly —

but to use it more effectively.

Conclusion

Fertilizer prices are no longer just a cost factor —

they are shaping the entire farm economy.

In 2026, profitability depends on how well farmers manage input costs.

Those who focus on efficiency and smart decision-making will remain profitable —

while others may struggle despite good crop prices.

Written by Janardan Tharkar – an agriculture content researcher and blogging professional with practical experience in farming education, digital publishing, and SEO content optimization. Janardan focuses on modern U.S. agriculture trends, smart farming technologies, irrigation systems, crop development, organic farming practices, and farmer-support programs to create helpful, practical, and trustworthy content for American readers.