The paradox at the heart of U.S. agriculture in 2026 is difficult to ignore: crop prices, on paper, look strong—yet farmers across major producing states are reporting tightening margins, rising financial stress, and growing uncertainty about the next planting season.

At a distance, the system appears healthy. Corn, soybeans, and wheat prices remain historically elevated compared to pre-2020 averages. Export demand is steady. Global supply risks still support price floors. But at ground level, the lived experience of farmers tells a very different story—one shaped not by price alone, but by the widening gap between revenue and cost, and by the growing tension between the key actors who shape agricultural outcomes.

This is not a simple margin squeeze. It is a system under strain.

The illusion of “high prices”

The assumption that high crop prices translate into farm profitability is rooted in an older cost structure—one where inputs were relatively stable and predictable. That assumption no longer holds.

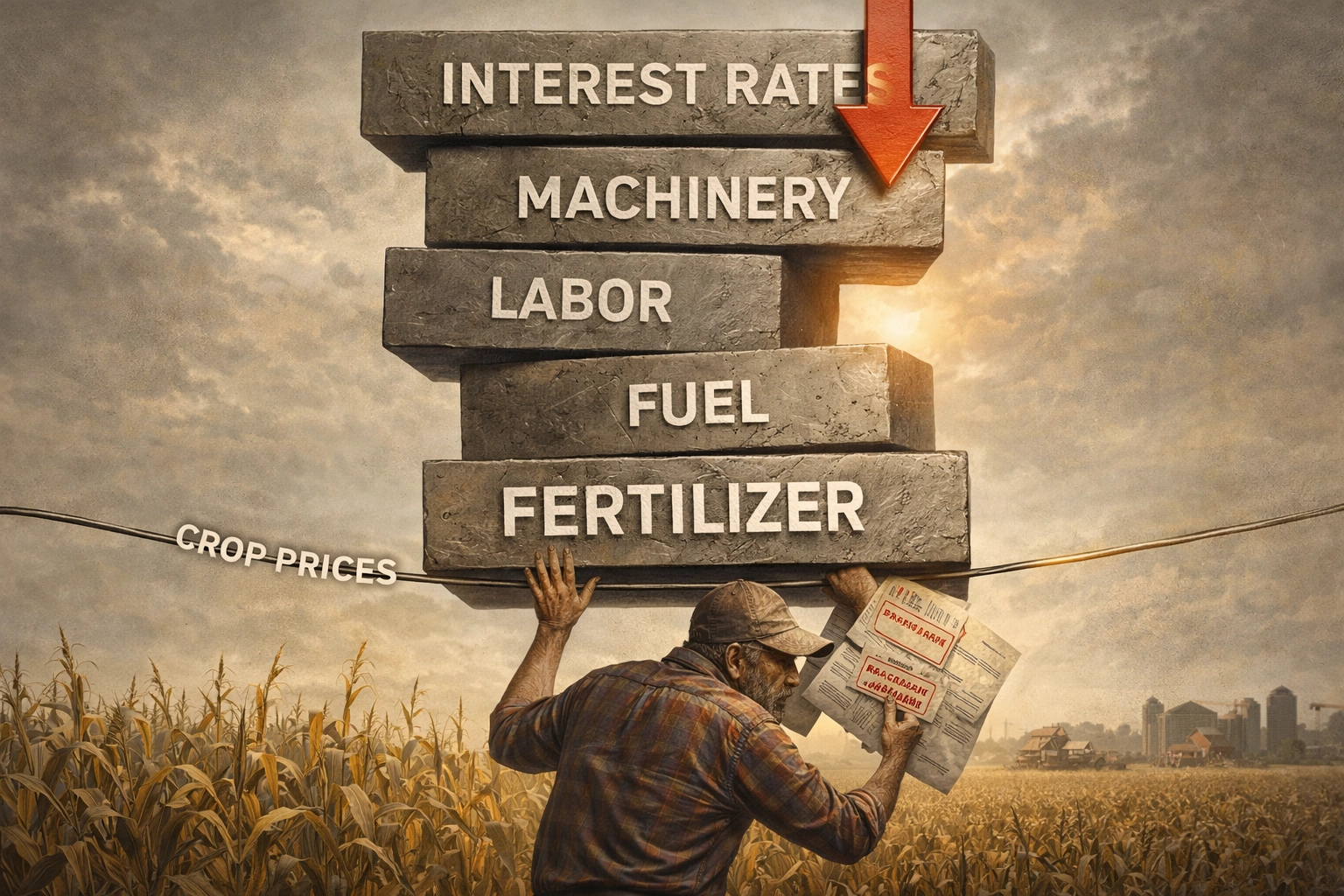

According to data and outlooks from the USDA Economic Research Service , while commodity prices have remained elevated, production expenses have risen at a faster and more volatile pace. Fertilizer, fuel, machinery, labor, and interest costs have all moved upward—often simultaneously.

The result is a deceptive equation:

High prices – Even higher costs = Compressed margins

Farmers are not struggling because prices are low. They are struggling because price signals are no longer reliable indicators of profitability.

This creates the first major tension:

👉 Markets suggest strength

👉 Farm balance sheets suggest stress

That disconnect is where confusion—and frustration—begins.

Where the pressure actually sits: the cost structure breakdown

To understand the strain, you have to look at the cost stack—not as isolated inputs, but as a layered system where multiple pressures reinforce each other.

- Fertilizer costs remain structurally elevated

- Fuel prices fluctuate with geopolitical risk

- Machinery costs have surged due to supply chain disruptions

- Interest rates have increased financing burdens

- Labor shortages push wages higher

Individually, each of these is manageable. Together, they form a compounding pressure system.

Industry coverage highlights how input inflation continues to erode farm profitability despite stable commodity prices.(https://www.reuters.com/business/agriculture/farmers-face-cost-squeeze-despite-strong-crop-prices-2026)

What makes 2026 different is not just the level of costs—it is the synchronization of cost pressures. Farmers are no longer able to offset one rising cost with stability in another.

If you want to better understand how rising input costs are transforming farm-level decisions, read our in-depth analysis “Why Fertilizer Prices Are Quietly Reshaping U.S. Farm Economics in 2026.” The article explains how fertilizer is no longer just a cost component, but a key constraint shaping profitability, cropping choices, and long-term farm strategy.

The grower–supplier tension: pricing power vs dependency

At the center of the conflict is a structural imbalance between farmers and input suppliers.

Large fertilizer, seed, and chemical companies operate with global pricing power. Farmers, by contrast, operate in localized markets with limited negotiating leverage.

This creates a recurring tension:

- Input suppliers adjust prices based on global supply-demand dynamics

- Farmers must absorb those costs regardless of local crop conditions

From the farmer’s perspective, this often feels like a one-sided equation:

👉 When input costs rise → farmers pay immediately

👉 When crop prices fall → farmers absorb the loss

There is no symmetrical protection mechanism.

Reports and commentary across agricultural media increasingly reflect this frustration, with farmers questioning pricing transparency and timing in input markets (see: https://www.farmprogress.com/management/farm-input-costs-pressure-2026).

This is not just an economic issue—it is a trust issue.

Farmers are beginning to question whether input pricing reflects true market conditions or strategic pricing behavior by large suppliers.

The policymaker gap: support that doesn’t align with reality

If the tension with suppliers is about pricing, the tension with policymakers is about alignment.

Government programs in the U.S. have historically been designed around price-based triggers—support mechanisms activate when crop prices fall below certain thresholds.

But in 2026, the problem is not low prices—it is high costs.

This creates a structural mismatch:

- Policy assumes price decline = risk

- Reality shows cost inflation = risk

As a result, many farmers fall into a policy blind spot:

👉 Prices are high enough to disqualify support

👉 Costs are high enough to erode profitability

This gap is increasingly discussed in policy analysis circles and agricultural policy debates (example: https://www.fb.org/market-intel/farm-income-and-cost-pressures-2026).

The frustration among growers is not just economic—it is institutional. There is a growing perception that policy frameworks are lagging behind the realities of modern agriculture.

Decision-making under pressure: what farmers are actually choosing

These tensions converge at the most critical point: farmer decision-making.

Every season, farmers must answer a set of increasingly difficult questions:

- Do I apply full fertilizer rates and risk higher costs?

- Do I cut inputs and risk lower yields?

- Do I switch crops based on input intensity?

- Do I lock in prices early or wait for better market signals?

These are no longer routine decisions—they are high-stakes economic bets.

The pressure is intensified by uncertainty. Input prices can change rapidly. Weather risks remain unpredictable. Global markets shift quickly.

This creates a decision environment defined by:

- Incomplete information

- High volatility

- Limited margin for error

Farmers are not just managing farms—they are managing risk portfolios.

As input costs continue to rise, decisions around nitrogen application are becoming less about maximizing yield and more about managing financial risk. This shift reflects a broader pressure across U.S. corn farming, where weather uncertainty and cost volatility are forcing farmers to rethink traditional strategies. A deeper look at this challenge can be found in

corn farmers under pressure in 2026: costs, weather, and planting strategy, where these economic and environmental factors come together to shape on-field decisions.

The communication breakdown: when signals stop working

A functioning agricultural system relies on clear signals:

- Prices signal demand

- Costs signal supply constraints

- Policy signals provide stability

In 2026, those signals are increasingly distorted.

- High crop prices signal opportunity—but costs negate that opportunity

- Input prices signal scarcity—but lack transparency

- Policy signals fail to reflect real risk conditions

This creates a communication breakdown across the system.

Farmers, suppliers, and policymakers are all responding to different signals—and often reaching conflicting conclusions.

The result is not just inefficiency—it is misalignment.

Real-world consequences: beyond the balance sheet

The impact of these tensions extends beyond farm profitability.

1. Input reduction and yield risk

Farmers cutting fertilizer and chemical use to control costs risk lower yields, which can tighten supply and increase volatility.

2. Farm consolidation pressure

Smaller and mid-sized farms, with less financial flexibility, face greater risk—accelerating consolidation trends.

3. Mental and financial stress

The uncertainty and pressure of decision-making are contributing to increased stress levels within farming communities.

4. Investment hesitation

Farmers delay capital investments in equipment and technology, slowing productivity growth.

5. Regional disparities

Areas with higher input costs or lower yield potential face disproportionate challenges.

These are not abstract outcomes—they are visible across rural America.

The global dimension: competitiveness under strain

U.S. agriculture does not operate in isolation.

When domestic cost structures rise, global competitiveness is affected.

Countries with:

- Lower input costs

- Favorable currency conditions

- Government support mechanisms

can gain an advantage in export markets.

The result is a subtle but important shift:

👉 U.S. farmers compete not just on yield—but on cost efficiency

Global agricultural outlooks from organizations like the Food and Agriculture Organization highlight how input cost disparities are influencing production patterns and trade flows.

Over time, this could reshape global market shares in key commodities.

While global supply estimates and market projections provide a broader outlook, the real impact of these shifts is felt at the field level. In regions like the U.S. Midwest, farmers are already facing difficult planting decisions due to excess soil moisture and narrow timing windows. This real-world challenge is explored in detail in

too wet to plant, too late to wait: the real decisions behind Midwest corn planting in 2026, where macro trends translate into high-stakes on-farm choices.

Where the system starts to bend: trust and coordination

At its core, the issue is not just economic—it is relational.

The agricultural system depends on coordination between:

- Farmers

- Input suppliers

- Policymakers

- Market institutions

When trust erodes, coordination breaks down.

Farmers begin to:

- Delay purchases

- Reduce input usage

- Question advisory recommendations

Suppliers face:

- Demand uncertainty

- Inventory challenges

Policymakers struggle with:

- Designing effective interventions

- Responding to rapidly changing conditions

The system becomes reactive rather than coordinated.

Pathways forward: what actually needs to change

Resolving these tensions does not require a single solution—it requires adjustments across the system.

1. Policy realignment toward cost-based support

Support mechanisms need to account for input cost inflation, not just output price declines.

2. Greater pricing transparency in input markets

Improved data visibility and communication from suppliers can help rebuild trust.

3. Risk management tools tailored to cost volatility

Insurance and hedging tools should evolve to cover input cost risks—not just yield or price risks.

4. Investment in efficiency technologies

Precision agriculture, soil health practices, and input optimization can reduce dependency on volatile inputs.

5. Strengthening farmer bargaining power

Cooperatives and collective purchasing models can improve negotiating leverage.

6. Better communication channels

Bridging the gap between farmers, policymakers, and suppliers requires more consistent and transparent dialogue.

Across the U.S. Corn Belt, planting decisions are increasingly tied to market signals and policy expectations. As explored in our in-depth Corn Belt field analysis, these choices reflect a complex mix of agronomy, economics, and timing.

A system in transition, not collapse

It is important to recognize that U.S. agriculture is not failing—it is transitioning.

The tensions visible in 2026 are symptoms of a system adjusting to:

- Globalized input markets

- Volatile energy dynamics

- Changing policy environments

- Increasing economic complexity

But transitions are rarely smooth.

They expose weaknesses, test relationships, and force difficult adjustments.

The real story behind the numbers

The headline story—high crop prices—suggests strength.

The underlying story—rising costs, strained relationships, and distorted signals—reveals stress.

Farmers are not struggling because markets are weak.

They are struggling because the system around them is out of alignment.

Until that alignment is restored—between prices and costs, between policy and reality, between suppliers and growers—the tension will remain.

And in agriculture, tension rarely stays contained. It reshapes decisions, restructures systems, and ultimately defines the future of the industry.

The events of 2026 may not look like a crisis in the traditional sense. But they mark something equally important:

A turning point in how agricultural economics actually works.

Written by Janardan Tharkar – an agriculture content researcher and blogging professional with practical experience in farming education, digital publishing, and SEO content optimization. Janardan focuses on modern U.S. agriculture trends, smart farming technologies, irrigation systems, crop development, organic farming practices, and farmer-support programs to create helpful, practical, and trustworthy content for American readers.