In the spring of 2026, the contradiction is everywhere.

Grocery bills remain stubbornly high. Shoppers in suburban supermarkets wince at the price of eggs, beef, lettuce, and cereal. Headline inflation may have cooled from its post-pandemic peak, but food-at-home prices are still elevated compared to pre-2020 norms. Yet across rural America, small U.S. farmers are quietly reporting thinner margins than they’ve seen in years.

Retail food prices are high. Farm-level margins are not.

The gap between what consumers pay and what small producers receive has become one of the defining tensions in American agriculture in 2026. It is not the result of a single failure or conspiracy. It is the outcome of macroeconomic forces, supply-chain concentration, financial tightening, and structural imbalances that increasingly separate farm-gate economics from supermarket pricing.

According to the U.S. Department of Agriculture’s Economic Research Service, the farm share of the consumer food dollar has hovered around roughly 14–16% in recent years, depending on the product category (USDA ERS Food Dollar Series). That means when a family spends $100 at the grocery store, farmers collectively receive only a fraction of that amount. The rest accrues to processing, packaging, transportation, marketing, and retail margins.

For small farmers — especially those without vertically integrated operations — that structural reality is becoming more painful in 2026.

High Prices, High Costs

At the macro level, the U.S. economy in 2026 remains defined by elevated interest rates relative to the pre-pandemic era, lingering wage inflation in labor-intensive sectors, and cautious consumer spending growth. The Federal Reserve’s tightening cycle earlier in the decade cooled headline inflation, but it also increased borrowing costs across industries — including agriculture.

Food retailers face higher labor and logistics costs. Processors absorb elevated energy and packaging expenses. These costs contribute to high retail prices. But they do not necessarily translate into higher farm-gate prices.

The disconnect arises because retail food inflation is driven primarily by downstream costs — distribution, branding, transportation, compliance — not necessarily by raw commodity prices.

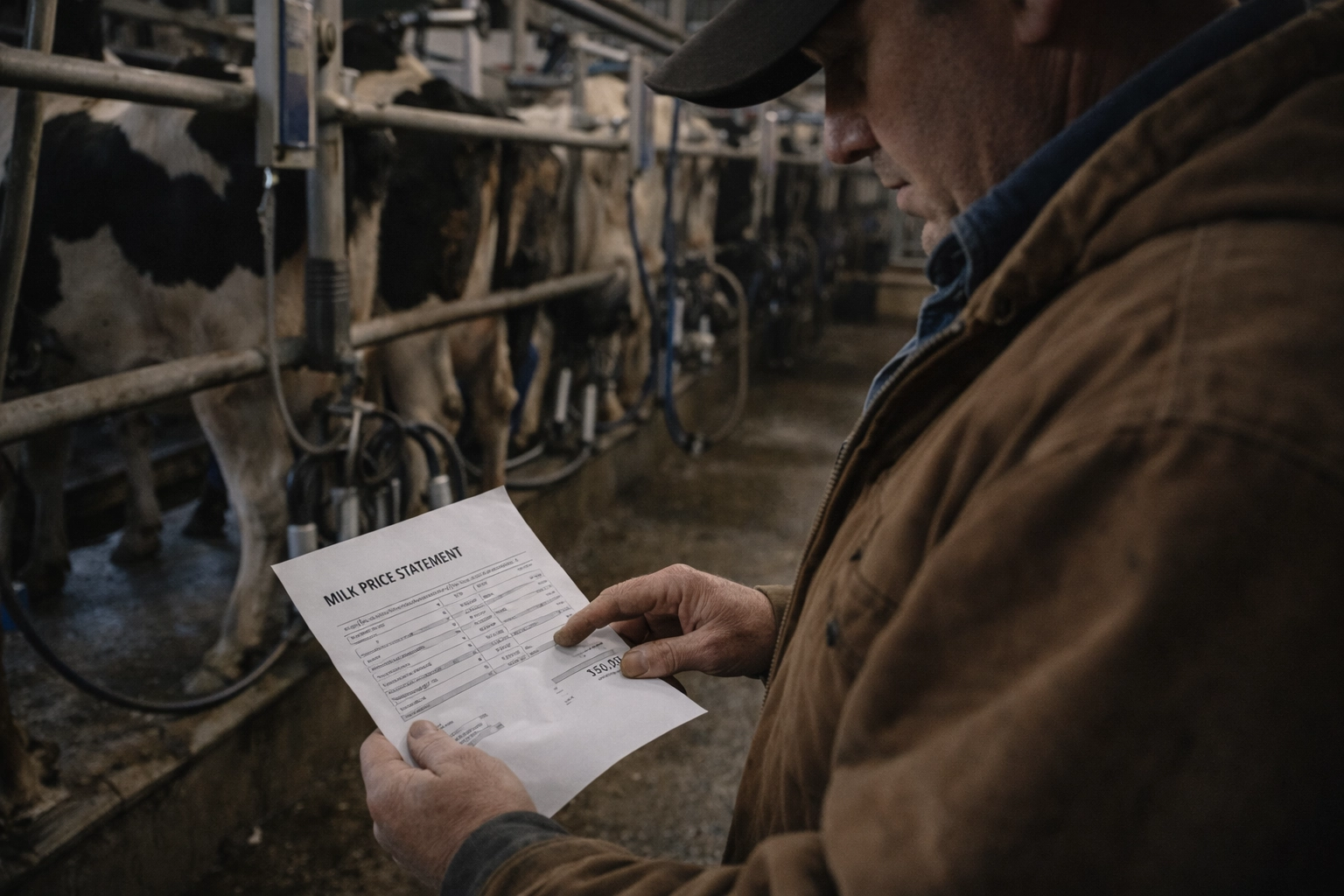

A small dairy producer in Wisconsin may see milk checks stagnate or decline, even as shoppers pay more for cheese and yogurt. A vegetable grower in California may struggle with labor and water costs, even as packaged salad prices rise in urban stores.

The farm share is thin. And when upstream input costs rise faster than farm-gate prices, margins collapse.

Net farm income is falling again in 2026 not because of a single shock, but because multiple macro forces are converging at once: normalized commodity prices, structurally higher input costs, rising real interest burdens, and a cooling global demand picture.

Where the Chain Breaks

To understand the squeeze, one must trace the supply-demand mechanics through the food system.

1. Commodity Normalization

Many commodity prices have moderated from their 2022 peaks. Grain markets stabilized as global supply chains recovered. Livestock prices fluctuate regionally, but feed costs, export competition, and herd cycles influence returns.

Small farmers often sell into commodity-linked markets, even if their products are differentiated. When corn or soybean prices normalize downward, livestock feed dynamics adjust. When milk production rises nationally, farm-level milk prices soften.

Meanwhile, grocery prices remain elevated due to:

- Higher labor costs in retail and food service.

- Packaging and processing expenses.

- Transportation and fuel costs.

- Corporate margin management amid volatile supply chains.

The Bureau of Labor Statistics’ consumer price data show persistent elevation in food-at-home categories compared to 2019 baselines (BLS Consumer Price Index). But farm-level revenue does not move in tandem with those retail adjustments.

2. Processing Concentration

Processing and distribution sectors are highly concentrated in certain commodities. Beef packing, poultry processing, and grain trading are dominated by a handful of firms.

Small producers lack leverage in pricing negotiations. They often operate as price takers, not price setters.

When retail prices rise, processors and retailers may capture much of the additional margin. Farm-gate prices may move marginally — or not at all.

This asymmetry is structural.

The Farm Share Problem

Small farms face a series of structural disadvantages that intensify margin loss in 2026:

- Limited economies of scale.

- Less bargaining power with processors.

- Higher per-unit compliance costs.

- Reduced access to hedging tools.

- Greater exposure to local labor market volatility.

The USDA’s farm income projections indicate overall sector income has moderated from earlier highs, but those aggregate figures mask disparities between large commercial operations and smaller farms (USDA Farm Income Forecast).

Large operations often hedge commodity exposure and negotiate volume-based contracts. Smaller producers rely more heavily on spot markets or regional buyers.

When the farm share of the food dollar remains low, any cost increase — fertilizer, seed, labor, insurance — cuts directly into net margin.

Similar decisions are playing out across US Agribusiness in early 2026. Grain handlers are postponing storage upgrades. Equipment manufacturers are tempering production plans.

Overview of Profit Margin Pressure

Midway through 2026, the imbalance can be summarized as follows:

| Category | Retail Level | Small Farm Level |

|---|---|---|

| Food Prices | Elevated vs. 2019 | Often flat or declining |

| Input Costs | Indirectly passed through | Directly absorbed |

| Bargaining Power | Concentrated retailers/processors | Fragmented producers |

| Access to Capital | Corporate credit lines | Higher-cost farm loans |

This comparison highlights why small farmers feel squeezed despite visible food inflation. Retailers can pass through cost increases. Processors can adjust margins. Small farmers cannot easily transfer higher costs downstream.

They absorb them.

The table reveals a structural misalignment: price strength exists in the system, but not where the margin pressure is greatest. Farmers operate at the narrowest point of the value chain.

Financial Leverage Strain

If cost inflation were the only challenge, farmers might adapt gradually. But 2026 brings capital pressure into sharper focus.

Interest rates remain significantly higher than they were in the 2010s. According to Federal Reserve agricultural finance reports, farm loan rates have climbed materially compared to the ultra-low period that preceded the pandemic (Federal Reserve agricultural finance data).

For small farmers, borrowing costs matter disproportionately.

Operating loans fund seed, feed, fertilizer, and labor. Equipment financing supports machinery replacement. Land mortgages represent long-term commitments.

When rates rise:

- Annual interest expenses increase.

- Debt service consumes a larger share of revenue.

- Cash flow flexibility shrinks.

Large integrated operations may secure more favorable credit terms due to scale and diversified revenue streams. Small producers face stricter underwriting and higher relative costs.

Debt itself is not catastrophic. But declining margins make debt heavier.

A vegetable grower who once reinvested surplus into irrigation upgrades may now postpone improvements. A livestock producer may delay herd expansion. A beginning farmer may abandon plans to purchase adjacent acreage.

These are not abstract shifts. They alter the structure of rural communities.

Across U.S. agriculture in 2026, generational transition has moved beyond a demographic talking point. It has become a structural risk factor—one that influences credit decisions, land markets, capital investment, and long-term production capacity.

Regulatory Environment

Federal farm programs offer safety nets, but they are often calibrated to commodity benchmarks rather than retail dynamics.

Price Loss Coverage and Agricultural Risk Coverage programs trigger payments when reference prices fall below thresholds. They do not respond to rising labor or compliance costs. Crop insurance protects against yield and revenue volatility, but it does not guarantee profitability.

The Congressional Budget Office’s agricultural baseline projections emphasize the interaction between market prices and federal outlays (CBO Agriculture Baseline). But for small diversified farms — specialty crops, direct-market producers, livestock operators — traditional commodity programs may offer limited support.

Meanwhile, regulatory compliance costs — environmental standards, labor regulations, food safety protocols — continue to evolve. Larger firms spread compliance costs across broader output. Small farms bear them more acutely.

Supply Chains and Scale

The pandemic years revealed fragility in centralized supply chains. Yet consolidation has not reversed significantly.

Large retailers leverage purchasing power to negotiate favorable contracts. Private-label branding expands margins for stores while compressing upstream prices.

Small farmers selling through wholesale channels often face “take it or leave it” contracts. Direct-to-consumer models — farmers markets, CSAs, online sales — offer higher margins but limited scale.

In 2026, consumer budgets are tighter. Premium local food markets grow more slowly than during peak pandemic demand. That reduces the cushion for small producers relying on differentiated pricing.

What It Looks Like on the Ground

The consequences of shrinking margins manifest quietly:

- Deferred machinery replacement.

- Reduced hired labor hours.

- Increased reliance on family labor.

- Scaling back acreage.

- Hesitation to adopt new technology.

Some small farmers pivot toward agritourism or value-added processing. Others exit production altogether.

Margin compression rarely announces itself with headlines. It accumulates over seasons.

Structural Changes Over Time

If current dynamics persist, several long-term shifts are likely:

1. Accelerated Consolidation

As small farms struggle with margin pressure and debt servicing, larger operations may acquire land and market share.

2. Expanded Vertical Integration

Producers may seek ownership stakes in processing or distribution to capture greater share of retail value.

3. Increased Financialization

Institutional investors may continue expanding farmland holdings, reshaping ownership patterns.

4. Policy Recalibration Pressure

Persistent margin stress may intensify calls for antitrust scrutiny in processing sectors or adjustments in farm support programs.

The Core Contradiction

The central paradox of 2026 is this:

Consumers see high food prices. Farmers see thin margins.

The explanation lies not in retail shelves, but in the structural layers between farm and fork — processing, transportation, branding, finance, and capital costs.

Small U.S. farmers are losing margin despite high retail food prices because they operate at the least powerful point in the value chain, while absorbing disproportionate cost increases and facing tighter credit conditions.

The grocery receipt does not tell the farm’s story.

That story is written in operating loans renewed at higher rates, fertilizer invoices paid upfront, and machinery repairs delayed another season.

If long-term structural reforms do not address bargaining asymmetry and cost pass-through limitations, margin pressure will remain a defining feature of small-scale American agriculture.

And in 2026, that pressure is no longer theoretical.

It is operational.

Written by Janardan Tharkar – an agriculture content researcher and blogging professional with practical experience in farming education, digital publishing, and SEO content optimization. Janardan focuses on modern U.S. agriculture trends, smart farming technologies, irrigation systems, crop development, organic farming practices, and farmer-support programs to create helpful, practical, and trustworthy content for American readers.